|

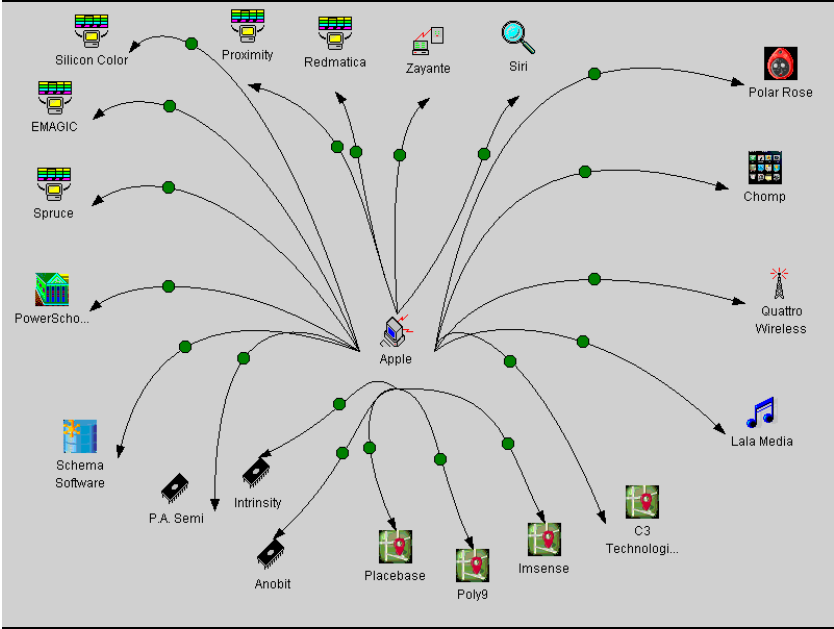

| Apple acquisitions since 2001 |

Apple has not been a particularly acquisitive company over this 12 year period. In contrast, Google acquired about twice as many companies in the year 2011 alone.

The infographic on the right depicts these 20 acquisitions, clustering the deals by market segment. You can view much more detail at Apple acquisitions since 2001.

Three clusters stand out: 1) Media application software (Spruce, EMAGIC, Silicon Color, Proximity and Redmatica). The most recent deal (Redmatica) develops applications used for sampling and editing audio files and for managing audio libraries; 2) Semiconductors (P.A. Semi, Intrinsity and Anobit). The most recent deal (Anobit) makes a key component that improves the performance of NAND flash memory chips, which are used in products such as iPhones, iPads, and iPods; 3) Mapping, imaging, drawing (Placebase, Poly9, Imsense, C3 Technologies). The most recent deal (C3) is a developer of three-dimensional mapping technology and now operates as the "Sputnik" division of Apple. This latter cluster of deals was particularly important as Apple moved away from using Google Maps in its new iOS 6.

Curiously, Redmatica (Italy), Anobit (Israel), and C3 Technologies (Sweden) were all headquartered outside of the US. Apple's M&A reach clearly has a global perspective.